LinkedIn

LinkedIn

Facebook

Facebook

X.com

X.com

WeChat

WeChat

Keep your cargo sailing smoothly, with valuable insights from our Asia-Pacific Market Update for December.

As 2023 approaches, the outlook is more pessimistic than optimistic as the possibility of a global recession weighs on sentiment. Falling trade growth, tighter monetary controls and weakening consumer demand all point to a tougher start to the New Year for the container shipping sector. But there are some bright spots too – port congestion especially in Europe and North America has been eased, largely ending the supply chain bottlenecks and disruption of the last couple of years.

China has also lifted virtually all its COVID-19 restrictions after abandoning its zero-COVID-19 policies of the last three years, raising the prospect of a trade resurgence, despite of a foreseeable impact of soaring positive cases.

Market Trends

Global growth continued to stall in November with key indicators all sliding. The Global Composite Purchasing Manager’s Index (PMI) nudged lower to 48 in November against 49 the previous month while the manufacturing orders-to-inventory ratio also slipped from October’s level suggesting the growth momentum deteriorated further. Manufacturing export order were again flat.

Inflationary pressures are still causing concern despite the possibility headline inflation in the US and Europe has peaked due to lower energy prices. Central banks, including the US Fed, continue to raise interest rates to rein in inflation although there are worries such action could plunge leading economies further into recession.

Trade Outlook

Cargo demand remains weak and this is expected to continue into 2023 due to a combination of high inventory levels and the likelihood of a global recession that could already be underway. Latest figures show container volumes continued to fall in most regions in July-September compared with the same period last year but were particularly weak on European and Asia trades. North American imports and West Central Asia exports were also witnessing certain level of decreasing.

Global container volumes fell 4.3% in July-September compared with a year earlier. The biggest fall was in intra-Europe volumes which crashed 12.5% in July-September from the previous year, followed by North American imports which dropped 9.3% and Asia imports which slumped 7.6%. But Oceania – Australia and New Zealand – was one of the few bright spots with export volumes growing 5.3% and imports rising 4.9% in July-September from a year ago.

Port delays in Europe and North America are also easing with Clarksons port congestion index for northern Europe and the US West Coast both seeing an improvement in congestion levels. Ocean spot freight rates are also falling and are now below those seen in the second half 2020 and are moving closer to pre-pandemic rates.

Trending Topic

Global Beef Trade is on the rise with an increased demand for beef imports in China. In the first three quarters of 2022, China imported 1.69 million tons of beef from all over the world, an increase of 200,000 tons from the same period in 2021. As of right now, the price of beef in the Chinese market stands at 65.80 Chinese Yuan per kilogram (equivalent to around 9.50 USD per kilogram), which adds up to only a one percent rise within the last year.

Meanwhile, across the equator in New Zealand, the export of protein has boomed. For example, in the single month of August 2022, New Zealand ports shipped 885 million USD worth of red meat, mostly to their three key markets of China, the United States, and Japan; a 34% increase since 2021. According to the Meat Industry Association, the import of beef to China from New Zealand has increased 49%. This means that monthly, China imports nearly 24,000 tons of beef from New Zealand, a record high that has not been seen since June 2019.

Click here to find out the factors leading to this current situation

Ocean Update

Maersk and IBM have agreed to end TradeLens, a blockchain-enabled global platform, that is expected to go offline by the end of Q1 2023. While action is taken to discontinue the platform, all parties involved in the process will ensure customers are attended to without disruptions to their business, Maersk said in a statement announcing the decision.

Rotem Hershko, A.P. Moller - Maersk Head of Business Platforms, said while Maersk-IBM developed a viable platform, the need for full global industry collaboration has not been achieved. “As a result, TradeLens has not reached the level of commercial viability necessary to continue work and meet the financial expectations as an independent business,” he said in the statement.

Maersk will continue its efforts to digitise the supply chain and increase industry innovation through other solutions to reduce trade friction and promote more global trade.

2022 has been a year of learnings, and in response to our customers’ needs for flexible and reliable ocean transportation, we have widened our contract product portfolio and customers can now choose the product that fit their business needs the best, be it fixed or floating rate, flexible space allocation etc., and I am confident this will improve the resilience of supply chains.

Key Market Outlook Across Trade Lanes

| Trade | Trade Statement | The most critical destination port situation update |

|---|---|---|

|

Trade

Asia Pacific - North Europe

|

Trade Statement

Maersk will continue its efforts to digitise the supply chain and increase industry innovation through other solutions to reduce trade friction and promote more global trade.

While we see a slightly stronger booking in pre-CNY, we expect overall demand in January to be flat. Customers tell us they are still suffering from super high DC stock levels and low consumer confidence when it comes to spending. |

The most critical destination port situation update

Key ports update:

Bremerhaven - MSC Gate: Yard density is stable at around 73% for dry cargo, 45% for reefer and 61% for IMO cargoes. Waiting time has been reduced to 0-12hrs although certain services are berthing on arrival with their best ETAs. Bremerhaven - NTB: Yard density is quite stable at 69% for dry freight and 45% for reefer. Rotterdam: Yard density is stable with an average 40% for dry cargo. |

|

Trade

Asia Pacific - Mediterranean

|

Trade Statement

December demand is healthy, and space is available. We will continue to take a proactive approach to ensure key corridors are well covered by alternative solutions in case congestion causes vessel delays.

|

The most critical destination port situation update

Below ports face 2-3 days of delay:

VALENCIA, SPAIN: Berthing line-up congestion with high yard density. SINES, LISBON & LEIXOES PORTUGAL: Terminals affected by a pilot strike which is causing some delay and congestion. PIRAEUS, GREECE: Some delays and congestion caused by a pilot strike. TRIESTE, ITALY: High yard density. RIJEKA, CROATIA: High yard density. KOPER, SLOVENIA: High yard density. CASABLANCA, MOROCCO: Berth line-up congested due to weather conditions. HAIFA, ISRAEL: Berthing line-up congestion. |

|

Trade

Asia Pacific - North America

|

Trade Statement

Overall, space is available from Asia Pacific to North America. We are observing a much stronger booking trend in December compared with the trend in recent weeks. The North American ports situation is improving, and our ambition is to maintain weekly service coverage in Q4.

USEC port congestion varies from port to port. Overall waiting time is 1-3 days, while Baltimore has decreased to 5 days and Houston congestion has lengthened to up to 5 days. Los Angeles and Long Beach have limited waiting time, which makes our LA/LB transit time the best-in-class in the market. In Vancouver, Maersk has collaborated with the terminal to minimize delays to less than a day, while the average waiting time in the market is still around 20-40 days. This makes our Vancouver and Price Rupert product transit time the most competitive in the market. We merged our TP1, TP9 and TP7 services into a new TP1 service in late October to relieve pressure on the Vancouver by streamlining port calls on all Pacific North-West services and we now expect to offer the best-in-class Asia to Canada products in the market. We have also merged TP23 to TP17 and TP3 to TPX and TP2 to offer customers a more stable and leaner product portfolio. With the upcoming CNY holiday, we encourage customers to plan ahead to avoid a space crunch resulting in supply chain disruption. |

The most critical destination port situation update

Overall USEC ports: 1-3 days waiting times

Savannah: 5-10 days Houston: 3-5 days Los Angeles/Long beach: 0-1 day waiting time. Oakland: 12-18 days Seattle: 1 day Prince Rupert and Vancouver: nil waiting time for Maersk |

|

Trade

Asia Pacific - Latin America

|

Trade Statement

West Coast South America

Overall network has space available to cater for the CNY cargo rush. We have products available to accommodate our customers’ demand from Asia to WCSA market. |

The most critical destination port situation update

Overall operating normally.

|

|

Trade

Asia Pacific - West Central Asia

|

Trade Statement

We see market demand to Middle East and India/Pakistan remaining flat, with demand still impacted by inflation, as well as economic situation in Pakistan/ Sri Lanka.

Overall we have product available to accommodate our customers’ demand from Asia Pacific to the West Central Asia market. |

The most critical destination port situation update

Overall operating normally

|

|

Trade

Asia Pacific - Africa

|

Trade Statement

Exports are picking up gradually from South China due to the easing of COVID-19 restrictions in Guangzhou. This, combined with the impact of the early CNY in January, means we suggest customers plan booking well in advance in the coming weeks.

Vessel schedule reliability is improving, especially on West Africa and South Africa services. We will continue to focus on further improvements to service delivery levels. |

The most critical destination port situation update

Waiting time:

Kribi: 2-4 days Matadi: 3-4 days Nouadhibou: 1-2 days Dar Es Salaam: 8-10 days Zanzibar: 14 days |

|

Trade

Asia Pacific - Oceania

|

Trade Statement

Space is available for destinations in Australia and New Zealand. Auckland metro port is experiencing business as usual. Due to the holidays, we encourage customers to plan ahead to avoid a space crunch.

|

The most critical destination port situation update

|

|

Trade

Oceania - World

|

Trade Statement

Supply chain disruptions remain in Oceania which impacts sailing schedules across the industry. Maersk continues to perform well ahead of the industry average on service reliability.

We have added additional vessels to our PANZ and Jstar services in the past month to increase buffer in the schedule. To improve schedule reliability and supply chain stability for our customers the Komodo service will be delayed l slide in week 49 and the Cobra service will also be delayed in week 1 have a slide in week 1 to reset schedules. To assist customers managing their cargo during the holiday season we recommend they consider our value added services on Maersk Spot where additional freetime can be purchased at a significant discount at the time of booking and selecting Maersk rollable for non-transit time sensitive cargo. |

The most critical destination port situation update

Tauranga port waiting time, on window is 0.5-2 days, off window is 11-15 days.

Sydney and Fremantle ports have waiting times of 3-4 days. |

|

Trade

Import - Asia Pacific

|

Trade Statement

Asia’s main ports are virtually delay-free with an average waiting time of around 0-2 days.

We have granted three extra free days for China import between January 21-23 during the CNY holiday to ease pressure on customers’ supply chain. China has eased COVID-19 control and quarantine measures so we see less risk of city lockdowns and port closures. |

The most critical destination port situation update

Maersk has further strengthened its ocean product to North China. Transit time and schedule reliability have significantly improved from various origins to Qingdao/Xingang/Dalian.

Feeder capacity has been upgraded to North East Asia and South East Asia. Most ports are open for booking acceptance. Maersk has deployed five dedicated express sailings for the coming Chile cherry season. We provide an integrated end-to-end cold chain solution to ensure cherries arrive swiftly and fresh. |

|

Trade

Intra - Asia

|

Trade Statement

Demand has been soften and production has been slow down in various parts of Asia due to the holidays season. In China, the operation and port productivity are closely monitored given the context of new measurements on Covid 19 and upcoming CNY holidays.

In Manila, there experiences a shortage of plugs in the terminal and transit/delivery time for the reefers units will be impacted. |

The most critical destination port situation update

|

Vertical Insight: Auto

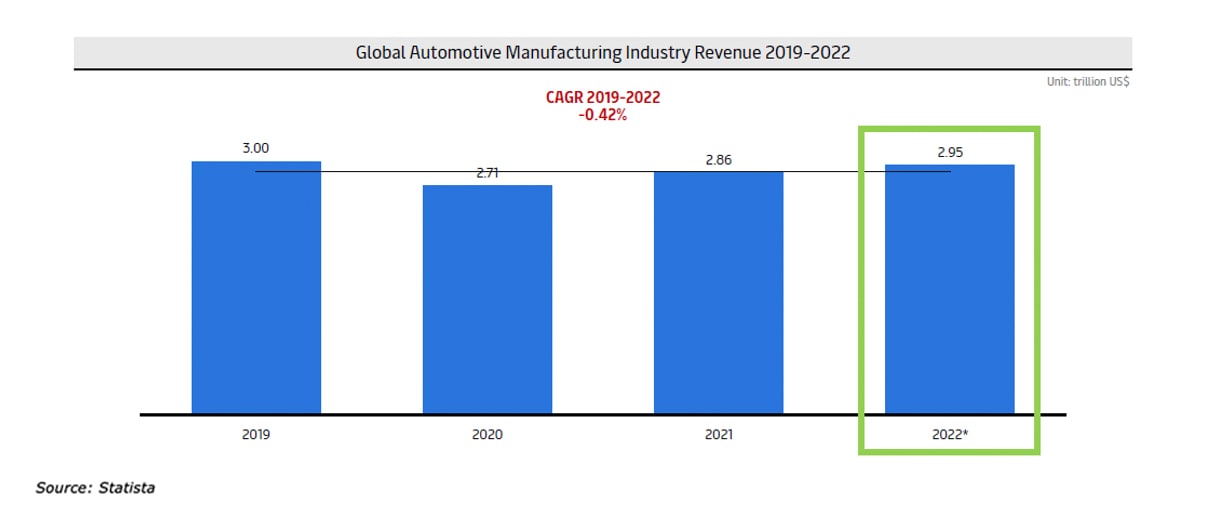

The global automotive manufacturing is projected to grow to US$ 2.95 trillion in 2022 the market is recovering from 2020-2021, but it is rather slow and still under 2019 market size.

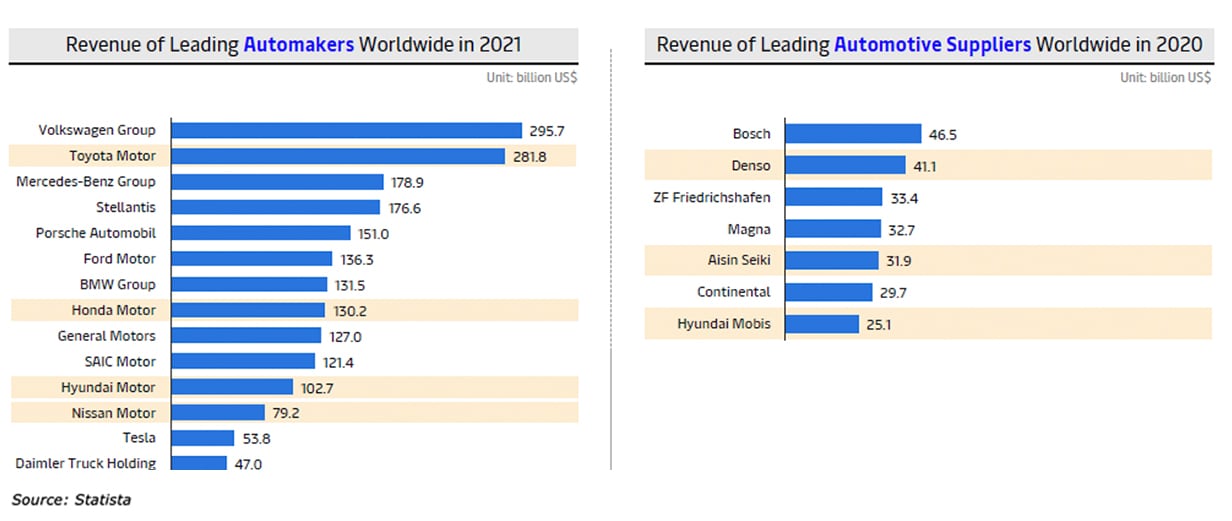

Among the global automotive manufacturers, 4 out of the top 15 OEM/Fully Built Car manufacturers, and 3 out of top 7 T1 component manufacturers are from Asia Pacific mostly from Japan and South Korea.

Japan and China are one of the key markets for both export and import (strong in both manufacturing & consumption); South Korea and Thailand are a big market for Export (strong in manufacturing) while Australia stands out from Import side (strong in consumption).

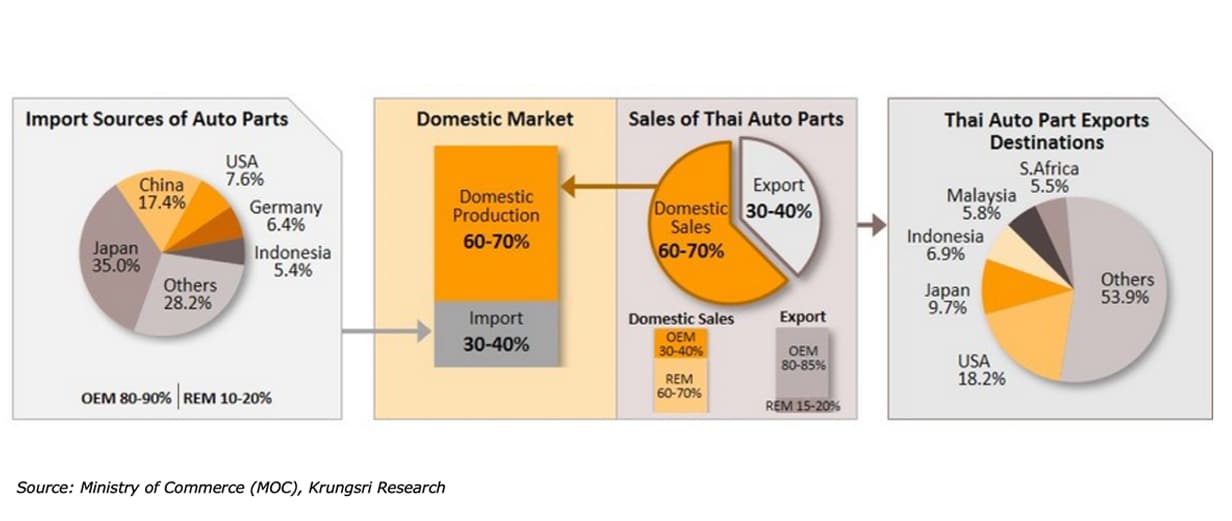

Thailand is the 13th largest automotive parts exporter and the 6th largest commercial vehicle manufacturer in the world, and the largest in ASEAN, which accounts for nearly 12% of the country’s economic growth and employs more than 500,000 people. Over a period of 50 years, the country has developed from an assembler of auto components into a top automotive manufacturing and export hub. Nearly, all top Japanese (30 companies) and Global (32 companies) component manufacturers have their production base in Thailand.

Thai automotive supply chain is highly domestic and intra-Asia. For the domestic market, nearly 60- 70% of components are consumed domestically. Even for 30-40% imports, 58% of them are sourced from the neighboring Asian countries (Japan, China and Indonesia). When exporting the auto parts, 1/5 of them are as well exported to the neighboring Asian countries (Japan, Indonesia and Malaysia).

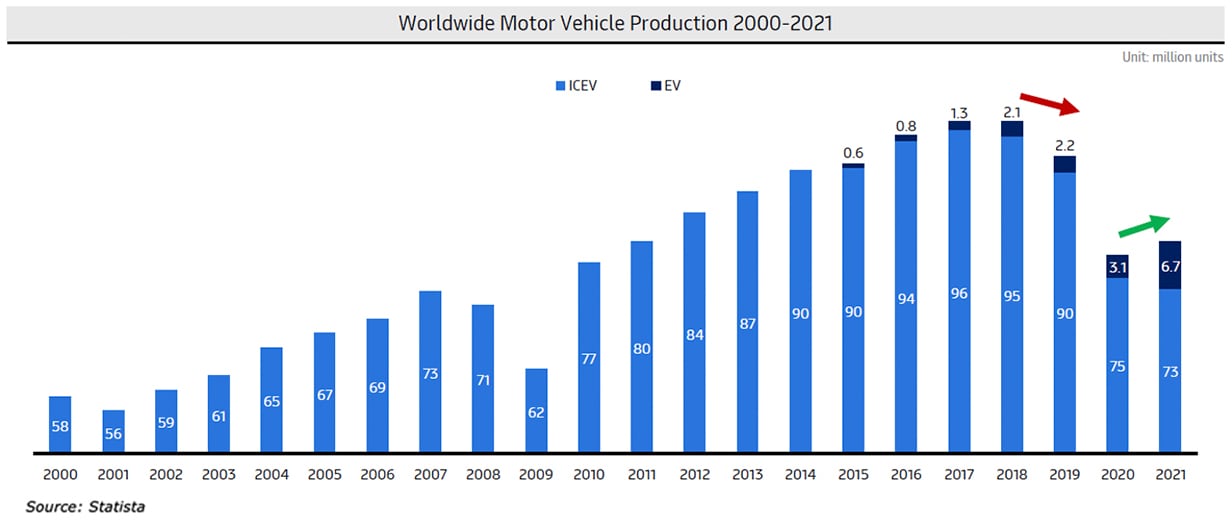

From 2019, the automobile production started falling with stagnating or contracting consumer demand; shifting from combustion engine to electric vehicle is expected to reignite global market growth.

In this transition, 4 out of the top 10 EV manufacturers come from Asia Pacific countries (led by China and South Korea), which reconfirms the importance of APA region for the growth and future success of Maersk.

In this transition, 4 out of the top 10 EV manufacturers come from Asia Pacific countries (led by China and South Korea), which reconfirms the importance of APA region for the growth and future success of Maersk.

The semiconductor shortage has escalated to impact all major OEMs and automotive manufacturing regions. The Society of Motor Manufacturers and Traders (SMMT) shows a decline of 99, 211 cars (32.4%) in the first three months of 2022 due to the semiconductor shortage plaguing the industry. Many industry experts now expect the shortages to persist throughout 2022 and into 2023, leaving little prospect to recover volumes.

While the chip shortage is the biggest headline, the industry is facing other upstream supply issues that could persist. There are shortages in commodities from leather and fabrics to steel and rubber, often because production has struggled to recover to pre-pandemic levels. Competing demand from other recovering industry verticals has also hurt automotive supply. Global surges in energy costs could even lead some smaller or niche suppliers to ration production. There are concerns of factory stoppages in China, for example, as the country tries to reduce coal consumption.

You can find solutions here to help remove the roadblock from your automotive supply chain. Please click here to find more insights that help steer your way to the UPSIDE of automotive change.

Air Update

Greater China: Hi-tech customers including Microsoft and Apple increased volume to the US, Europe and Australia since the end of November which has affected airline utilization during the period.

Airfreight rates from China to the US and Europe are more than 50% cheaper that the corresponding period last year.

Japan: The number of freighter flights from Japan in December exceeded 250 flights per week for the first time in about six months.

All Nippon Airways will adjust its US and East Asian routes from December with an increase in the number of flights between Narita to Chicago, Shanghai, Beijing, Taipei and Incheon but a reduction in flight frequency to Los Angeles and Bangkok. The approach of the New Year holidays is likely to see a reduction in the number of air cargo related flights.

Japan Airlines saw a 13% reduction in international air cargo volumes to 41,000 tons, the fourth straight month of declines.

Inland Services Update

Greater China: Maersk has launched new rail corridors from Shenyang to provide an alternative for our customers in the North-East region and our key client BMW does ship volume with us on this corridor.

We have new sea-rail product feature on SPOT, which is an important step on our digital journey and feedback from both external and internal customers is very positive.

Warehouse operations in mainland China, Hong Kong and Taiwan are all working normally despite the COVID-19 situation.

Japan: Container drayage capacity is stable although we expect a peak season before and after the New Year. Construction on the Tokyo-Nagoya highway is causing delays with can affect delivery times in the Kanto/Tokai areas.

Philippine: Vessel waiting times at the Manila terminals have increased to an average of 2 days due to bad weather and the pre-Christmas and CNY peak season. The delays are expected to increase as most industries prepare for the holiday break and ports close for 24- hours for Christmas and New Year.

Major Ports Update

Vessel Waiting Time Indicator

| Less than 1 day | 1-3 days | More than 3 days | |

|---|---|---|---|

|

Asia Ports

|

Less than 1 day

Busan, Xingang,

Shanghai, Ningbo,

Shekou, Xiamen,

Yantian, Nansha,Chiwan,

Hong Kong, Singapore,

Tanjung Pelepas

|

1-3 days

Qingdao, Brisbane,

Auckland

|

More than 3 days

Tauranga, Lyttelton

|

|

Rest of World

|

Less than 1 day

Bremerhaven,

Felixstowe, Long Beach,

Los Angeles, Apapa, Tin

Can, Tema, Lome, Onne,

Dakar, Conakry, Maputo,

Balboa

|

1-3 days

Vancouver, Newark,

Miami, Poti, Valencia,

Sines, Abidjan, Luanda,

Pointe Noire

|

More than 3 days

Koper, Port Tangier,

Oakland, Savannah,

Houston, Cotonou, Kribi,

Matadi, Dar Es Salaam,

Zanzibar

|

Remark: Numbers are dynamic and subject to change.

Resources and tools to support you

Visit our “Insights” pages where we explore the latest trends in supply chain digitization, decarbonisation, growth, resilience, and integrated logistics.

Learn what’s happening in our regions by reading our Maersk Europe, North America and Latin America updates.

Visit us at Maersk.com to handle everything from “Last Free Day” to online payments.

We value your business and welcome your feedback. Should you have any questions on optimizing your cargo flows, please contact your local Maersk professional.

Anything you need, we’re here to help

Logistics services

Contact us

Ready to ship?

I agree to receive logistics related news and marketing updates by email, phone, messaging services (e.g. WhatsApp) and other digital platforms, including but not limited to social media (e.g., LinkedIn) from A. P. Moller-Maersk and its affiliated companies (see latest company overview). I understand that I can opt out of such Maersk communications at any time by clicking the unsubscribe link. To see how we use your personal data, please read our Privacy Notification.

By completing this form, you confirm that you agree to the use of your personal data by Maersk as described in our Privacy Notification.